Early this year, a video of 19-year-old Daniel Iskandar being washed like a corpse as ‘punishment’ for stealing a donation box in a Selangor mosque went viral. The video initially sparked public outrage, but perceptions quickly changed when news broke that the teen was found to be positive for drugs at the time of the recording. He was swiftly labelled with derogatory terms such as ‘kaki dadah’ and ‘penagih’.

Reactions towards Daniel’s case is just one example of the long-standing stigma towards Persons Who Use Drugs (PWUDs) in Malaysia. His case is not isolated; similar reactions can also be seen, for example, to a 7-minute video published by local NGO Peluang in which a PWUD shares her traumatic experience with the country’s legal process after committing a minor drug offence.

* We previously wrote about the impact of the over-incarceration of minor drug offenders on prison overcrowding in Malaysia here.

Person Who Use Drugs (PWUD) is an umbrella term that encompasses the spectrum of drug users ranging from minor drug offenders to drug users who suffer from substance abuse or addiction disorder.

Negative public perception towards PWUDs is hardly anything surprising in Malaysia, where decades of a war on drugs waged by authorities have inevitably left a lasting impression on the people. This sentiment, however, comes with consequences that go far beyond name-calling; research on the impact of stigma against PWUDs show that it significantly harms their recovery as well as reintegration into society.

Malaysia is not the only country with a history of a tough approach towards drugs. Ever since President Richard Nixon declared drugs as America’s ‘public enemy number one’ in 1971, countries around the world have followed suit and waged their own wars against drugs. A key aspect to supporting the anti-drug campaign has been messaging, which has helped shape negative public opinion towards not only drugs, but also drug dependents and drug offenders. Policy documents, traditional media, and – nowadays – social media are some of the channels through which this sentiment has been shaped. Research has shown that wars on drugs are sustained through rigorous messages in government campaigns and the media, which in turn are used to justify harsher penalties for drug offences.

In Malaysia, ever since drugs were declared as the ‘Main Threat to Society’ in 1983, the government’s messaging effort has focused on creating a hostile rhetoric towards drugs through the adoption of fear tactics — as seen in national campaigns such as ‘The More You Use The Less You Live’ and ‘Perangi Dadah Habis-Habisan’. To date, the national policy on drugs still reflects the same, punitive narrative towards drug use which tends to frame PWUDs as potential criminals who would commit crime to finance their addiction.

Such narratives do not end at the policy level. Media reports of PWUD-related cases have long been profiling them as potential criminals or socially problematic individuals by nature. An analysis of 904 drug-related news articles that we conducted between August 2019 and January 2020 — after former Health Minister Datuk Seri Dr. Dzulkefly Ahmad announced the Pakatan Harapan government’s plan to decriminalise drug possession for personal use — shows that media attention is primarily focused on the criminal aspect of drug-related issues; we found that 41% of news reports are on capture and arrest, 28% on raids by law enforcement, and only a mere 7% covered drug policy related topics:

On top of that, around 21% of all news reports highlight drug use prominently despite it being an indicidental factor to other crimes; 12% of all news reports also highlight the convict’s previous drug charges, further framing and suggesting an association between ‘drugs’ and ‘crime’ to the audience. While it has been some time since our analysis was conducted, recent headlines suggest that our findings unfortunately still hold.

Such messaging approaches, both by the government and the media, only stand to reinforce an already hardened societal stigma towards PWUDs. A 2020 study found that stigmatising language such as ‘addicts’ and ‘abusers’ create more barriers for PWUDs to either get help or reintegrate into society. In the case of Malaysia, PWUDs struggle to access opportunities such as employment, education, housing, and loans. Stories from formerly incarcerated PWUDs would describe the hardship they face in finding shelter after being released from prison, causing them to go homeless. With the lack of social support, many end up reverting to old habits — as reflected in the steady increase of recidivism rate among drug offenders in Malaysia since 2015.

Today, as policymakers consider more science-backed and rehabilitative approaches to dealing with drug-related issues in Malaysia, we believe that the way PWUDs are portrayed in government and media messaging efforts should also change. As a start, there is a need to be more discerning about the socioeconomic factors that contribute to drug use – an aspect the news media tend to overlook when reporting on drug related matters. A more holistic and constructive reporting method when it comes to drug related matters could help change the way society views PWUDs. As observed in the case of Canada, reforming the way the media reports news (by emphasising public health instead of crime perspectives when reporting on drug cases, for example) can and does bring about shifts in public discourse about drugs and PWUDs.

Understanding the factors associated with drug use – socioeconomic (as mentioned above) as well as demographic – would also give policymakers a chance to better strategise their preventive effort in the future and tailor more fitting preventive programs to different targeted populations. It could be a first step towards eliminating societal stigma surrounding PWUDs.

Beyond preventive efforts, education is key in the long run. Educating the public with facts about drugs could empower them to form more informed opinions. This approach brought about a favourable outcome in Iceland, where the country saw a significant reduction of adolescent substance abuse after incorporating a multifaceted prevention program at the school level. The Icelandic government not only focused on compulsory substance abuse education, but also emphasised on strengthening community and family support networks through various state-sponsored after school programs — something we could perhaps learn from to foster a more inclusive and rehabilitative environment for PWUDs.

Ultimately, people hear what they are told to hear when it comes to drugs and PWUDs. It will undeniably take considerable effort to reform the way we think about them as a society, but one that is important and long overdue. Until this changes, however, we should remember that those like Daniel deserve empathy, not derogation.

Home affordability is a perennial issue affecting Malaysians, particularly young Malaysians. Aspects of the affordability issue have been frequently highlighted, including by The Centre in a primer published last year. One key fact worth reiterating here is the yawning chasm between median house prices and annual median household income – this disparity has nearly tripled from 2002 to 2019.

Even so, every consecutive Malaysian administration has continued to encourage home ownership. Most housing-related policies – ranging from subsidised home loans to large-scale government-subsidised projects like PR1MA – have focused on supplying homes for purchase and reducing obstacles to home ownership, especially for the younger generation.

However, given long-standing stagnant wages and rising household debt levels, should home ownership continue to be the overwhelming focus of government housing policy? Or should greater policy attention be directed towards those who cannot afford to buy a house and have resorted to renting, such as the proposed Residential Tenancy Act? And finally, might there be shifts in housing preferences towards long-term renting, especially by the young, if there were greater protections and incentives?

These are the questions we ask in our new research series which delves into Malaysian youths’ housing aspirations. We seek to understand the push and pull factors associated with home renting versus home owning. We also aim to recommend policies befitting a fair society comprising both renters and owners.

In this first instalment of the research series, we first look into the ownership versus renting landscape in Malaysia, and present findings from a preliminary poll on housing aspirations.

Home ownership and housing policy in Malaysia

Like many countries around the world, home ownership is the predominant mode of housing1 in Malaysia. The 2019 Household Income and Basic Amenities Survey shows that home ownership in Malaysia is high and has continued to rise since 2010, albeit slowly: from 72.5% in 2010, to 76.3% in 2016, and most recently to 76.9% in 20192.

Within the context of Southeast Asia, the rate of home ownership in Malaysia is not unusual; only the Philippines has a lower home ownership rate at 64.1% (2019). Other ASEAN neighbours have comparably high rates of home ownership such as Thailand (77.4%, 2010), Indonesia (81.1%, 2021), Myanmar (85.5%, 2014), Vietnam (88.1%, 2019) and Singapore (88.9%, 2020)3.

Malaysia’s and these ASEAN countries’ home ownership rates are quite high in comparison to developed countries such as the United States (65.5%, 2021), the United Kingdom (65.2%, 2018), Japan (61.2%, 2018), Germany (50.4%, 2020), and France (64.0%, 2020). Switzerland, interestingly, only has a 42.3% home ownership rate (2020)!4

In the 1960s, the Malaysian government’s housing priority had largely focused on providing shelter for low-income households especially in urban areas. Public-funded low-cost housing, such as the Projek Perumahan Rakyat (PPR), allowed low-income households to rent or own a property at a subsidised cost.5 After the New Economic Policy was introduced in 1970, a 30% Bumiputera quota for the sale of new housing stock, as well as a 5 percent discount, were introduced to facilitate the community’s urbanisation and home ownership.

As the Malaysian middle class continued to grow in number, the demand for better affordable housing continued to rise in tandem, driven by an environment of rising house prices and cost of living. This has led to a significant shift in government policy over the past two decades – ensuring supply and ownership of homes not only among low-income households, but also among middle-income families.

Apart from increasing the supply of ‘affordable’ housing via new programs such as PR1MA, various financing incentives were introduced to facilitate ownership such as the My First Home Scheme6, Youth Housing Scheme, the Home Ownership Campaign7, the Private Affordable Ownership Housing Scheme (MyHome)8 and MyDeposit.

However, Malaysia’s household debt has risen to levels unseen before, from only 47% of GDP in 2000 to 93% in 2020. Given these high levels of household debt – which are likely an understatement of total household borrowings9 – it is questionable whether further policy support towards home ownership via easier financing is a good idea.

The ‘hidden’ renter-households

Malaysia’s relatively high home ownership rate masks an important fact: there is a significant proportion of households that do not own homes in the Klang Valley. As of 2019, home ownership rates in Selangor and Kuala Lumpur are 69.7% and 63.3% respectively, which are considerably lower than the national average of 76.9% (Figure 1).

Breaking down the data according to household income reveals a more stark reality. Only 52.5% and 45.3% of B40 households in Selangor and Kuala Lumpur own their own homes, which is much lower than the average home ownership rate for B40 households nationally which stands at 73.1% (Figure 2).10

The picture is similar for M40 Klang Valley households; only 65.4% and 51.2% M40 households in Selangor and Kuala Lumpur respectively own the homes that they live in. In comparison, the home ownership rate for M40 households nationally is 75.5%.

At higher incomes however, the home ownership gap between Klang Valley households and Malaysia overall closes. Overall, 87.0% of Malaysia’s T20 households own homes compared to 86.6% of T20 households in Selangor and 77.9% in Kuala Lumpur.

Thus, the data shows that a sizable proportion of B40 and M40 households in Klang Valley are renting relative to the rest of the country. Renting is likely driven by the lack of affordability in particular locations but are there other factors at play? To get a fuller picture of renting patterns and its determinants, we collaborated with market research firm Dattel on a short poll in January 2022 comprising an urban sample of 809 respondents.

Who rents?

Geography

Our short January 2022 poll presented a pattern similar to DOSM’s 2019 home ownership data, though because our sample is mainly concentrated in urban centres, it resulted in smaller differences between regions. The poll results showed that renting is more prevalent in Klang Valley (41.0%), the South Peninsular states (38.4%) and East Malaysia (35.1%). This is followed by those living in East Peninsular states (27.3%) and North Peninsular states (26.6%) (Figure 3). In all regions, except for North Peninsular and East Peninsular, the percentage of respondents who are renting is higher than those living in their own homes.

In terms of home ownership, the highest percentage is among respondents from North Peninsular states at 37.3%. This is followed by East Peninsular states (34.9%), South Peninsular states (31.7%), Klang Valley (29.3%) and East Malaysia (24.0%).

Respondents who are staying with their parents or relatives are quite substantial in all regions, ranging from 26.3% in South Peninsular to 36.6% in East Malaysia.

Age

Unsurprisingly, renting is higher among younger respondents compared to older respondents. 38.9% of respondents aged 20-29 are currently renting, followed by those aged 30-39 at 35.4% (Figure 4). It is interesting to note that a quite significant proportion of older respondents, i.e. those aged between 40 and 59, are also renting. The survey found that 34.1% and 25.9% of respondents aged 40-49 and 50-59 respectively are currently renting their homes.

A substantial percentage of younger respondents are staying with their parents or relatives. 45.8% and 31.2% of respondents aged 20-29 and 30-39 respectively do so compared to much lower rates among respondents aged 40-49 (20.2%) and 50-59 (5.8%). Staying with relatives become more common again among the oldest respondent band, those aged 60-69 (18.6%), perhaps due to ageing and caregiving needs.

Unsurprisingly, home ownership increases with age. The percentage of respondents who live in their own property is 42.8% for 40-49 age group, 60.7% for 50-59, and 67.6% for 60-69 compared to 12.2% and 30.5% among the 20-29 and 30-39 age groups respectively.

Top Reasons for Renting

The biggest reason for renting is the unaffordability of down payment, cited by 44.5% of respondents who are currently renting (Figure 5). However, preferring to live in a particular location is also a relatively big reason, chosen by 23.9% of renting respondents. 17.2% of renting respondents said that they were unable to qualify for a home loan. And lastly, 7.2% of renting respondents said they chose to rent due to the flexibility it offers.

Unaffordability of down payment is the clearest reason for renting across all age groups, except for the 40-49 age band (Figure 6). Location preference is a relatively important reason for the 30-39 age band as well as the 40-49 age band compared to other age groups. Inability to qualify for home loans is not a top reason across all age groups, which runs counter to many policy prescriptions on loosening loan qualifying criteria. Flexibility is the least chosen reason among most age groups though curiously, it is quite an important reason for the 50-59 age group (the small sample size of renters within this age group may be one reason for this result).

While down payment unaffordability is the most cited reason in all regions (36.2% to 48.4%), location preferences is quite an important reason for renting in Klang Valley (30.7%) and East Malaysia (25.1%) (Figure 7). Meanwhile, inability to qualify for a home loan is a relatively strong reason in South Peninsular (25.2%) and East Peninsular states (28.5%), compared to other regions.

Flexibility, curiously, is quite a significant reason for renting in the North Peninsular (14.2%) and East Malaysia (14.1%). One possible reason could be that respondents in those regions do not have a long-term residence expectation and plan to relocate to other, perhaps more urbanised, regions in the future.

Future Housing Aspirations

Overall, 44.3% of respondents aspire to buy their own home while 27.4% intend to continue living in their own home. 12.7% of respondents plan to stay indefinitely with their parents or relatives, while 12.0% look to rent long-term as a housing option.

Aspiration towards home ownership is higher among younger respondents at 59.7% and 46.0% among the 20-29 and 30-39 age groups followed by 38.0% of 40-49 years old respondents (Figure 8). The proportion drops drastically for respondents aged 50 and above, at 13.5% and 8.3% for the 50-59 and 60-69 age groups – unsurprisingly, given higher rates of home ownership amongst older respondents.

Therefore, it is also not surprising that the percentage of respondents who want to continue living in their own home is higher in older age groups. 70.6% and 65.6% of 60-69 and 50-59 years old respondents want to continue living in their own home. The figure drops to 38.5% among 40-49 years old respondents, followed by 24.8% among the 30-39 age group and 6.7% among the 20-29 age group.

Renting long-term is not a popular choice among younger respondents compared to older respondents, which we found surprising. Long-term renting as an option makes up only 12.4% and 13.7% respectively for the 20-29 and 30-39 age groups. A relatively high proportion of respondents aged 50-59, however, do intend to rent long-term (18.3%).

The preference for home ownership holds when we look at the responses from the perspective of regional location. Respondents with plans to buy a home or continue living in one’s property range from 69.1% to 78.2% across all regions (Figure 9).

The same predominance in preference for home ownership holds when we look at the pattern across gender categories. It is interesting to note that the percentage of male respondents (14.9%) who intend to rent long-term is higher than the percentage of female respondents (9.0%) (Figure 10).

Conclusion

The policy bias towards home ownership is a common one, particularly amongst Asian countries. One reason is home ownership’s tangible wealth effect, as property prices tend to appreciate in the long-run. Asian societies also traditionally view home ownership as a positional good which provides respectable social standing. From the policymakers’ perspective, home ownership contributes to social stability and rootedness in a state or country.

And yet, this policy bias is not without problems. Societal pressures towards home ownership, in a situation of relatively high house prices and stagnant wages, would likely result in even more unsustainable levels of household debt and stress. The bias towards home ownership also arguably takes away policy attention on making rents affordable and fair.

Based on DOSM data and our short preliminary poll, there is a significant segment of Malaysians who do not own homes, mostly out of necessity, but some also out of choice. Overzealousness in promoting home ownership will neglect the needs of citizens who are currently renting, and may ignore the needs of changing values around long-term renting in future.

Policy attention should not be confined to ‘upgrading’ tenants to homeowners, particularly when renting disproportionately affects low-income families in the cities; half of B40 families in Klang Valley are renting, perhaps for the foreseeable future, and thus require greater renter protection. Attention must be directed towards strengthening the legal and institutional frameworks underlying the rental market, which was also pointed out by Bank Negara Malaysia back in 2017.

The government is beginning to make this a priority. The Ministry of Housing and Local Government is proposing an enactment of the Residential Tenancy Act to prepare legal provisions to protect homeowners’ and tenants’ rights, prepare a uniform template for residential tenancy agreements, and to resolve disputes between parties involved in residential-tenancy transactions. Interestingly, it includes a proposal to create a new government entity to handle security deposits. While the enactment is in its early consultative phase (and has received pushback from developers and landlords amongst others), it is a timely intervention to regulate this long-neglected area.

In Part 2 of this research series, we will look into policies adopted by other countries and cities to make renting a viable long-term practice. Stay tuned.

It must be noted that in Malaysia, the official home ownership rate includes informal housing, which is defined as houses built without development orders (i.e. this includes houses illegally built on non-private lands or on river bank reserves, or “kampung” houses built by the local community.) Such houses are common in rural areas, and are usually built haphazardly without complying to approved housing standards and regulations. Nevertheless, they are still considered as part of the stock of household-owned homes in the official data. This may not be the case for other countries.

Source: 2010 figure, Khazanah Research Institute (2015); 2016 figure, Department of Statistics Malaysia’s Household Income and Basic Amenities 2016 Survey.

Projek Perumahan Rakyat (PPR) flats can be rented for RM128 per month, or bought for RM35,000 in Peninsular Malaysia and RM42,000 in West Malaysia. Prospective tenants or owners must meet certain eligibility criteria such as a household income not exceeding RM3,000 per month.

The My First Home Scheme, introduced in the 2011 Budget, allowed first-time buyers to obtain loan financing up to 110% of the purchase price without needing to pay any down payment. This scheme was guaranteed by Cagamas, the National Mortgage Corporation.

The Home Ownership Campaign, first introduced in 2019, and eventually extended to December 2021, was introduced to encourage home ownership by reducing cost of property purchase. Qualified participants would enjoy full exemption on stamp duty for properties up to RM1 million, partial exemption on stamp duty for properties up to RM2.5 million, and Instrument of Securing Loan stamp duty exemption for properties of up to RM2.5 million. On top of that, buyers can enjoy a 10% discount for properties listed under the scheme.

The MyHome scheme, introduced in the 2014 Budget and lasted until November 2020, allowed eligible homebuyers to have their down payment paid by the government. The MyDeposit scheme, introduced in 2016 and which lasted until October 2021, offered a rebate of 10% of the house price or RM30,000, whichever was lower, to first-house buyers of properties priced below RM500,000.

Unclassified borrowings such as ‘buy now pay later’ schemes are not yet included in household borrowing statistics

B40, M40, and T20 Malaysia refer to the household income classification in Malaysia. B40 represents the Bottom 40%, M40 represents the middle 40%, whereas T20 represents the top 20% of Malaysian household income.

Dalam Bahagian 1 siri penyelidikan ini, kami menggariskan masalah-masalah pokok tentang hutang pinjaman pendidikan di Malaysia. Untuk menampung usaha pengkorporatan universiti awam dan perkembangan pesat universiti swasta, pinjaman pendidikan diperkenalkan untuk membiayai kos pendidikan tinggi serentak dengan perkembangan bilangan pelajar. Sejak penubuhan PTPTN pada 1997, sebanyak RM62.5 bilion pinjaman pendidikan telah dikeluarkan kepada 3.5 juta peminjam. Keadaan ini mungkin munasabah sekiranya negara dan masyarakat mendapat pulangan positif secara meluas daripada pendidikan tinggi. Walau bagaimanapun, mobiliti sosial tidak direalisasikan secara sekata. Dalam erti kata yang lain, ramai peminjam tidak mendapat pekerjaan dan pendapatan yang setimpal dengan pendidikan mereka.

Dalam Bahagian 2, kami mengemukakan tiga dasar progresif untuk menangani isu berkaitan dengan hutang pinjaman pendidikan yang tertunggak pada masa ini: penghapusan pinjaman atau pengampunan hutang pendidikan secara bersasar, pembayaran balik berasaskan pendapatan, dan pengawasan yang lebih meluas terhadap operasi dan pembiayaan PTPTN. Mengkategorikan para peminjam mengikut keupayaan mereka untuk membayar balik merupakan tonggak utama cadangan-cadangan ini.

Dalam bahagian ketiga ini, kami melontarkan beberapa idea untuk memperbaharui cara rakyat Malaysia membiayai pendidikan tinggi mereka. Antara intipati penting dalam perbincangan ini adalah perlunya kita menyedari bahawa landskap pendidikan tinggi kini kian berubah, dan ijazah tradisional bukan lagi satu-satunya jalan untuk mendapatkan pendidikan tinggi. Satu lagi aspek penting pembaharuan ini adalah perubahan yang diperlukan dalam struktur institusi, atau bagaimana untuk menyemak semula kaedah pembiayaan pendidikan. Selanjutnya, idea pembaharuan kami turut melibatkan cadangan untuk menyediakan langkah pembiayaan pendidikan yang lebih adil untuk keluarga yang kurang berkemampuan supaya kebergantungan meluas kita pada pinjaman pendidikan dapat dikurangkan.

Dalam artikel-artikel sebelum ini, kami telah soroti laporan media mengenai graduan dan anak muda Malaysia yang terperangkap dalam pekerjaan bergaji rendah selepas mengumpul hutang pendidikan yang besar untuk membiayai pengajian tinggi mereka. Ini konsisten dengan survei yang kami jalankan dari Ogos hingga September 2021. Satu pertiga daripada responden kami berkata pendidikan mereka tidak berbaloi dengan hutang pendidikan yang ditanggung. 59% berkata hutang pinjaman pendidikan menyumbang kepada tekanan kewangan manakala 57% berkata hutang pinjaman pendidikan menyumbang kepada kelewatan membeli rumah. 77% daripada responden bersetuju bahawa anak muda tidak sepatutnya perlu berhutang untuk mencapai pendidikan tinggi, dan majoriti yang lebih besar, 82% berpendapat bahawa tidak wajar golongan miskin perlu berhutang.

Beban hutang pinjaman pendidikan mendapat perhatian dalam Bajet 2022, di mana diskaun pembayaran balik telah diumumkan. Walaupun ia adalah petanda positif bahawa kerajaan memberi perhatian kepada isu pinjaman pendidikan, diskaun yang ditawarkan lebih bermanfaat untuk peminjam yang mempunyai kemampuan untuk membuat penyelesaian pinjaman yang besar atau untuk peminjam yang mampu membuat potongan gaji berjadual. Secara ringkasnya, ia memanfaatkan peminjam yang sudah pun mempunyai kemampuan kewangan. Diskaun-diskaun tersebut – yang sebenarnya diulang daripada pengumuman sebuah Belanjawan yang terdahulu – mencerminkan corak pemikiran dasar yang telah lama wujud tentang pinjaman pendidikan tinggi. Kami berpendapat bahawa sudah tiba masanya corak pemikiran ini dipertimbangkan semula secocok dengan perkembangan semasa.

Daripada ijazah tradisional kepada TVET dan mikrokredential

Antara pertimbangan utama dalam cadangan kami ialah trend pendidikan yang semakin beralih daripada program ijazah tradisional. Di Amerika dan UK, para pelajar dan ibu bapa sudah mula mempersoalkan pengajian ijazah tradisional dan sama ada kos untuk mengikutinya masih lagi berbaloi. Pandemik COVID-19 mungkin hanya akan mempercepatkan perkembangan ini dan menjadi punca kepada penurunan mendadak pendaftaran pelajar akhir-akhir ini.

Malaysia secara beransur-ansur bakal menghadapi keadaan yang sama. COVID-19 telah memburukkan, tetapi tidak menyebabkan, trend pengangguran siswazah dan gaji rendah siswazah. Pengangguran siswazah meningkat 22.5% kepada 202,400 pada 2020 daripada 165,200 pada 2019. Lebih merisaukan, nampaknya tren ini telah menaik sejak sekurang-kurangnya empat tahun lepas: pengangguran siswazah berjumlah 162,000 pada 2018, meningkat daripada 154,900 pada 2017. Ia juga memberi kesan yang signifikan kepada siswazah Bumiputera yang menghadapi kadar pengangguran yang agak tinggi.

Di samping kadar pengangguran, siswazah turut berhadapan dengan masalah gaji rendah; survei oleh Kementerian Pengajian Tinggi telah mendapati bahawa terdapat siswazah yang memperoleh gaji serendah RM1,000-1,500 sebulan. Bandingkan hasil ini dengan masa dan komitmen kewangan program ijazah yang biasanya mengambil masa sekurang-kurangnya empat tahun untuk diselesaikan. Program diploma tidaklah jauh lebih singkat – ia mengambil masa kira-kira 24-36 bulan untuk disiapkan dan lebih lama lagi jika dilakukan secara sambilan.

Mengambil kira situasi tukar-ganti dasar (policy trade-off) ini, penggubal dasar harus melakar semula corak pemikiran dasar yang memihak kepada ijazah akademik tradisional. Menuntut ilmu melalui ijazah adalah matlamat yang patut dipuji, tetapi adakah ijazah tradisional masih pilihan yang tepat untuk semua pelajar lepasan sekolah? Jawapannya adalah tidak, jika kita mengambil iktibar daripada pengalaman negara maju. Ramai lepasan sekolah mungkin boleh mendapat lebih manfaat – dan menjimatkan banyak masa dan wang – dengan mendaftar dalam latihan teknikal, program perantisan ‘belajar sambil bekerja’, kursus jangka pendek, skim kemahiran semula, kursus kelayakan mikro (mikrokredential), pembelajaran sepanjang hayat atau gabungan pilihan-pilihan ini.

Selain daripada pertimbangan kewangan, peralihan daripada ijazah tradisional juga didorong oleh perubahan landskap pekerjaan. Lepasan sekolah hari ini boleh membina portfolio mereka untuk bekerja sendiri ataupun bekerja bebas (freelance) berbanding dengan mendaftar di kolej untuk membina resume mereka untuk pekerjaan sepenuh masa.

Pemerhati dasar pendidikan Malaysia telah lama mengagumi Pendidikan dan Latihan Teknikal dan Vokasional (TVET) di negara lain seperti Sweden dan Jerman, di mana sistem TVET melatih pelajar untuk pelbagai bidang pekerjaan. Kadar pekerjaan bagi mereka yang mempunyai ijazah vokasional di negara-negara ini hampir sama tinggi dengan pemegang ijazah sarjana muda.

Kebolehpasaran graduan TVET juga tinggi di Malaysia, di mana ia mencapai kadar 98% dalam beberapa tahun kebelakangan. Ini jelas merupakan prestasi yang lebih baik daripada rakan-rakan mereka yang memegang ijazah. Pada tahun 2020, Pengarah Bahagian TVET, Azman Adnan dari Kementerian Pengajian Tinggi berkata bahawa kolej vokasional adalah penyedia terbesar pekerja berkemahiran di negara ini dan bahawa TVET adalah penyelesaian kepada ketidakpadanan kemahiran (skills mismatch) dan isu pengangguran siswazah.

TVET lebih murah, lebih pendek dan lebih dekat dengan keperluan industri. Walaubagaimanapun, tumpuan dasar dan peruntukan sumber pada TVET masih belum mencapai tahap yang diterima oleh sistem ijazah tradisional.

Namu begitu, terdapat beberapa usaha untuk mendorong perkembangan TVET dalam beberapa tahun ini. Dalam Rancangan Malaysia Ke-12, kerajaan bercadang untuk mengukuhkan program-program TVET dengan menaik taraf ekosistem industri, menambah baik akreditasi, mewujudkan sistem penarafan institusi TVET, dan mempromosikan platform berpusat yang menunjukkan data mengenai tawaran pekerjaan. Di bawah Bajet 2021, kerajaan telah memperuntukkan RM60 juta untuk Sistem Latihan Dual Nasional (SLDN), skim latihan yang berasaskan kompetensi dan berorientasikan industri. Elaun SLDN juga dinaikkan daripada RM600 kepada RM1,000 bagi menggalakkan lebih ramai peserta daripada isi rumah B40. Peruntukan keseluruhan untuk TVET juga telah meningkat daripada RM6 bilion dalam Bajet 2021 kepada RM6.6 bilion dalam Bajet 2022, sekali gus mencerminkan peningkatan penekanan kerajaan pada TVET.

Walau bagaimanapun, banyak lagi perlu dilakukan. Laporan Ketua Audit Negara 2019 mendapati program TVET yang dibiayai kerajaan secara keseluruhannya tidak mencapai sasaran Rancangan Malaysia Ke-11, malah sekadar menghasilkan separuh daripada jumlah graduan yang diunjurkan. Pendaftaran juga makin menurun dari 2016 hingga 2020, sungguhpun pandemik COVID-19 pastinya merupakan faktor penyumbang memandangkan banyak program TVET memerlukan latihan bersemuka.

Fragmentasi program dan pentadbiran TVET turut menjadi masalah. Institusi TVET dibiayai oleh kerajaan melalui enam kementerian, dan masalah pemecahan ini telah dibangkitkan sebelum ini dan keperluan untuk penyelarasan yang lebih baik telah diakui oleh kedua-dua kerajaan Pakatan Harapan dan Perikatan Nasional. Selain dari isu ‘penyelarasan’, rombakan besar dalam tadbir urus, perancangan dasar dan jaminan kualiti masih belum dilaksanakan walaupun keperluan berbuat demikian telah dibangkitkan beberapa kali, termasuk oleh Ahli Parlimen Nurul Izzah Anwar yang pernah berkhidmat sebagai pengerusi Jawatankuasa Pemerkasaan TVET.

Untuk mengangkat kepentingan TVET dan letak duduknya supaya setaraf dengan program ijazah dan institusi tradisional, kerajaan perlu melaksanakan pembaharuan struktur. Di Singapura dan Vietnam, hanya satu entiti menyelia sistem TVET negara masing-masing. Malahan dalam kes Vietnam, terdapat undang-undang khusus mengenai pendidikan vokasional, yang membolehkan kerajaan Vietnam melabur dengan secara substansial dalam TVET serta menggalakkan penyertaan sektor swasta melalui insentif percukaian, kredit, tanah, dan latihan para pendidik.

Walaupun mempunyai populasi yang jauh lebih kecil dan hanya lapan institusi TVET, Singapura mempunyai lebih 113,000 enrolmen pelajar TVET, angka yang setanding dengan jumlah enrolmen di politeknik dan kolej komuniti di Malaysia. Ini selaras dengan tinjauan KRI yang mendapati kurang daripada 10% belia di Malaysia mendaftar di politeknik TVET (tidak termasuk pusat latihan kemahiran) selepas pendidikan menengah.

Selain daripada TVET, kita juga harus memberi penekanan dan sumber kepada kursus latihan semula dan peningkatan kemahiran jangka pendek. Ini termasuklah apa yang dipanggil kelayakan mikro (mikrokredential). Berbanding dengan ijazah tradisional dan sijil TVET, kursus mikrokredential adalah lebih pendek, lebih fleksibel, dan lebih tertumpu pada kemahiran atau topik tertentu. Ia boleh ditawarkan dalam talian, secara bersemuka, atau melalui gabungan kedua-duanya.

Di Malaysia, naratif dasar sekitar pembangunan kemahiran dan mikrokredential telah disasarkan terutamanya kepada golongan dewasa yang bekerja. Pembiayaan adalah terikat dengan agensi seperti Kumpulan Wang Pembangunan Sumber Manusia (HRDF), Skim Insurans Pekerjaan di bawah PERKESO, dan Perbadanan Ekonomi Digital Malaysia (MDEC). Seperti mana TVET perlu diperluaskan, naratif dasar untuk pembangunan kemahiran dan mikrokredential juga harus dikembangkan kepada golongan lepasan sekolah.

Bukan semua pelajar lepasan sekolah pasti tentang apa yang mereka ingin belajar atau kerjaya yang ingin mereka ceburi. Mikrokredential menawarkan peluang untuk menguji minat bidang atau kerjaya tertentu sebelum melabur masa dan komitmen kewangan yang besar. Kerajaan boleh memberi insentif untuk menggalakkan tren ini. Contohnya, program SGUnited Skills di Singapura bukan sahaja menawarkan akses kepada pelbagai kursus latihan pendek bersubsidi untuk kemahiran dalam permintaan dan baru muncul (in-demand and emerging skills), ia juga menawarkan sokongan nasihat kerjaya dan elaun latihan bulanan sebanyak SGD1,200 sepanjang tempoh kursus untuk membantu menampung perbelanjaan hidup.

Dalam bahagian ini, kami telah menyatakan pendirian kami akan keperluan untuk dasar yang memihak kepada pemilikan ijazah tradisional sekarang beralih kepada pembangunan sistem sokongan dan promosi TVET serta kursus pembangunan kemahiran pendek atau mikrokredential di kalangan pelajar lepasan sekolah. Kami berpendapat bahawa keberhutangan pinjaman pendidikan di kalangan golongan muda sebahagiannya didorong oleh persepsi status dan andaian pulangan positif daripada pemilikan ijazah. Andaian ini perlu dikaji semula bukan sahaja oleh penggubal dasar tetapi juga oleh para majikan. Tenaga kerja muda hari ini berhadapan dengan inflasi ijazah, atau permintaan untuk ijazah sarjana muda dalam pekerjaan yang tidak benar-benar memerlukannya. Peralihan dasar ke arah TVET dan pembangunan kemahiran juga perlu disertakan dengan usaha untuk mengemas kini majikan mengenai penetapan kriteria kelayakan yang lebih relevan dengan keperluan semasa.

Beralih dari model pinjaman kepada subsidi terus untuk pelajar B40

Kerajaan semakin menggalakkan simpanan awal sebagai cara untuk membiayai pengajian tinggi. Ini merupakan langkah yang baik. Walau bagaimanapun, insentif dasar untuk menggalakkan simpanan pendidikan berkemungkinan akan lebih dimanfaatkan oleh keluarga berpendapatan pertengahan ke tinggi yang mampu menyediakan wang untuk tujuan ini. Bagaimana pula dengan isi rumah yang tidak mampu untuk menabung?

Kita harus beralih daripada pendekatan yang meminta keluarga B40 bergantung pada pinjaman pendidikan dan mempertimbangkan kaedah subsidi secara langsung. Pertama sekali, beban hutang pinjaman pendidikan nampaknya memberi kesan yang tidak seimbang kepada peminjam B40. Pengerusi PTPTN, menggunakan rekod badan itu sendiri, menulis bahawa meskipun hanya 55% daripada peminjam PTPTN datang daripada isi rumah B40, seramai 97% daripada peminjam lalai (yang tidak dapat membuat pembayaran balik secara konsisten) adalah daripada kumpulan pendapatan B40.

Kedua, seperti yang kami gariskan dalam Bahagian 1 siri kajian ini, kerajaan dan pembayar cukai sudah pun membiayai sebahagian besar pendidikan peminjam-peminjam PTPTN dengan membayar jurang kadar faedah antara kadar subsidi PTPTN kepada peminjam mereka dan kadar faedah pasaran yang dikenakan terhadap PTPTN atas pinjaman yang mereka ambil dari institusi kewangan. Memansuhkan pendekatan yang agak berpusing-pusing untuk mensubsidi pendidikan seseorang ini – dengan cara menggantikan subsidi faedah yang dibayar kepada institusi kewangan dengan pemberian subsidi tuisyen dan kos sara hidup secara terus untuk lepasan sekolah B40 adalah satu langkah yang lebih wajar dan bijaksana. Ia juga memberi manfaat kepada pengurusan PTPTN kerana ia memberikan sedikit kelegaan daripada menguruskan sebahagian besar peminjam yang berkemungkinan besar menjadi penghutang lalai.

Berapakah kos yang diperlukan untuk melaksanakan cadangan ini? Anggaran kasar kami meletakkan kos subsidi langsung pada 1.3-2 kali ganda lebih tinggi daripada kaedah semasa mensubsidi pinjaman pendidikan dan secara konservatif mengandaikan bahawa semua kursus yang dibiayai adalah untuk program ijazah dan dengan nisbah pelajar IPTS yang agak tinggi. Kos untuk subsidi langsung ini mungkin lebih rendah dengan adanya skim sokongan untuk pelajar IPTA serta peralihan daripada program ijazah tradisional kepada program diploma, TVET dan mikrokredential.

Gratuidad ialah program yuran (tuisyen) percuma bersasar yang dilaksanakan di negara Chile. Polisi ini digubal selepas bertahun-tahun protes mahasiswa terhadap kenaikan yuran dan lambakan hutang pinjaman pendidikan. Gratuidad menyediakan tuisyen percuma kepada pelajar dari 60% isi rumah terbawah. Subsidi tuisyen ditentukan oleh formula yang membahagikan institusi pendidikan kepada kategori mengikut tempoh pentauliahan mereka (sebagai proksi untuk kualiti) dan kemudian menetapkan tuisyen terkawal untuk setiap kumpulan dan setiap program pengajian.

Subsidi yuran pengajian dan kos sara hidup pelajar B40 bukan semestinya hanya datang daripada kerajaan dan pembayar cukai. Syarikat, yayasan persendirian dan individu berkemampuan tinggi juga boleh diberi insentif untuk menyumbang dan menambah kepada subsidi langsung ini. Dalam bahagian seterusnya, kami majukan komponen terakhir dalam cadangan pembaharuan pembiayaan pendidikan kami untuk memudahkan simpanan pendidikan di Malaysia supaya menjadi satu kelaziman sosial.

Daripada skim terputus kepada akaun pembelajaran sepanjang hayat (APSH)

Dewasa ini, seseorang warga Malaysia boleh membuat simpanan pendidikan melalui SSPN-i; memohon pinjaman daripada PTPTN atau PTPK; mencarum kepada HRDF, KWSP (Akaun 2), atau EIS; atau mengenalpasti tawaran agensi yang berbeza-beza dan mengambil kursus bersubsidi daripada MDEC, MARA, TEKUN dan banyak lagi.

Bagaimana jika ada cara yang lebih baik untuk membiayai pendidikan lepasan menengah seseorang sehingga usia tua? Cara yang menampung simpanan awal oleh ibu bapa serta subsidi langsung oleh kerajaan dan caruman atau biasiswa daripada bakal majikan atau dermawan? Kaedah yang mengikat dana tersebut dengan rakyat Malaysia secara individu dan bukannya dengan agensi latihan tertentu?

Menggabungkan kedua-dua pertimbangan di atas, kami mencadangkan akaun pembelajaran sepanjang hayat (APSH) untuk setiap rakyat Malaysia yang diuruskan sebagai dana pelaburan yang serupa dengan KWSP. Akaun tersebut hanya boleh digunakan untuk tujuan pendidikan, termasuk kos sara hidup. Dana itu disediakan secara automatik semasa kelahiran, dan setiap anak yang lahir di Malaysia akan menerima RM100 yang dikreditkan ke APSH mereka semasa pendaftaran kelahiran. Kanak-kanak yang dilahirkan dalam isi rumah B40 boleh dikreditkan dengan jumlah yang lebih tinggi bergantung pada tahap pendapatan isi rumah.

Akaun ini akan menjadi kaedah utama untuk skim simpanan sukarela yang diberi insentif oleh kerajaan untuk perbelanjaan pendidikan masa depan kanak-kanak itu, sekali gus menggabungkan ciri ADAM50 dan SSPN hari ini. Akaun ini juga akan menjadi tempat deposit untuk sebarang subsidi kerajaan untuk tujuan pendidikan dan latihan kemahiran pada masa hadapan, termasuklah pemberian insentif untuk program kemahiran semula (reskilling), sama seperti program SkillsFuture yang disediakan oleh kerajaan Singapura. Akaun tersebut juga boleh menerima pindahan daripada Akaun 2 KWSP serta deposit oleh agensi kerajaan, yayasan swasta, dermawan, atau bakal majikan untuk menyokong pendidikan pasca menengah, sama ada pinjaman atau biasiswa untuk program ijazah, diploma, TVET, mikrokredential, perantisan dan lain-lain kursus pembelajaran atau peningkatan kemahiran pada masa hadapan.

PTPTN barangkali berada pada kedudukan terbaik untuk mengendalikan urus tadbir dana ini memandangkan mereka telah pun menguruskan SSPN dan merupakan entiti yang bertanggungjawab mempromosikan tabungan pendidikan. Bagaimanapun, PTPTN perlu distruktur semula untuk menambah baik tadbir urusnya dan meluaskan mandatnya. Pelantikan ke dalam lembaga pengarah PTPTN hendaklah sama ketat prosesnya dengan pelantikan ke dalam lembaga pengarah KWSP untuk menjamin lembaga pengarah yang berkelayakan, cekap dan berautonomi. Untuk penyelarasan yang lebih baik, Perbadanan Tabung Pembangunan Kemahiran atau PTPK dan HRDF boleh digabungkan dengan PTPTN untuk mewujudkan suatu superfund yang berfokus untuk mengurus kewangan bagi pembelajaran sepanjang hayat.

Kerajaan Malaysia telah memperkenalkan pelepasan cukai untuk majikan (tamat pada 31 Disember 2021) yang membantu membayar pinjaman pelajar pekerja-pekerja mereka. Sekiranya rakyat Malaysia mempunyai akaun pembelajaran sepanjang hayat individu, insentif sedemikian juga boleh ditawarkan kepada individu dan syarikat yang menyumbang ke dalam akaun tersebut.

Kesimpulan

Melabur sejumlah wang dan masa untuk mendapatkan pengajian tinggi adalah satu keputusan kewangan yang besar. Untuk mengurangkan ketidaksamaan, kita perlu mengakui bahawa keputusan ini lebih berisiko terutamanya untuk segmen masyarakat yang kurang bernasib baik. Siri kajian kami ini telah menunjukkan kesan-kesan baik dan buruk apabila masyarakat bergantung pada pinjaman untuk membiayai pengajian tinggi. Walaupun pinjaman pendidikan telah meningkatkan akses kepada universiti dan kolej, ia memerangkap ramai graduan dalam hutang terutamanya mereka daripada isi rumah B40. Hal ini diburukkan dengan prospek kerjaya dan gaji yang tidak menentu dalam keadaan ekonomi negara yang masih rapuh.

Dengan mengambil kira latar belakang ini, kami menyokong untuk kerajaan mewujudkan subsidi terus dan elaun kos sara hidup untuk lepasan sekolah B40. Program ijazah tradisional (yang agak panjang dan mahal) bukan semestinya laluan yang terbaik untuk semua orang. Malah ia tidak lagi menjamin mobiliti sosial. Alternatif yang kurang diberi penekanan ialah TVET, yang sepatutnya mendapat tumpuan, sokongan dan promosi yang lebih besar. Kursus pembangunan kemahiran pendek atau mikrokredential juga harus digalakkan, bukan sahaja di kalangan orang dewasa yang bekerja tetapi juga di kalangan lepasan sekolah.

Untuk mengurangkan kebergantungan pada pinjaman pendidikan dan menjadikan simpanan pendidikan sebagai satu kelaziman sosial, kami juga mencadangkan agar akaun pembelajaran sepanjang hayat (APSH) diwujudkan secara automatik. Pendaftaran APSH automatik ini (opt out berbanding opt in) akan menjadi kaedah utama untuk skim simpanan sukarela yang diberi insentif oleh kerajaan, serta sebarang insentif tunai atau baucar untuk tujuan pendidikan.

Sebagai penjelasan, kami tidak mempersoalkan nilai pendidikan tinggi. Tetapi kita mesti mempertimbangkan semula cara kita mentakrifkan pendidikan tinggi dan cara kita membiayainya. Melangkah ke hadapan, kita harus merangka dasar untuk meningkatkan akses kepada pendidikan berkualiti (pengetahuan, kemahiran dan latihan teknikal), terutamanya untuk golongan yang kurang berada, tanpa mendorong mereka untuk menanggung hutang yang membebankan.

Cadangan-cadangan dasar kami sama sekali tidak menyeluruh, tetapi ia menawarkan corak pemikiran dasar yang baharu yang berorientasikan masa depan, berpandangan jauh dan lebih murah dalam usaha kerajaan meningkatkan akses kepada pendidikan tinggi. Pandemik COVID-19 telah memustahakkan lagi keperluan untuk menangani ketidaksamaan, dan ini merupakan satu kesempatan untuk merangka dasar pendidikan yang lebih baik, terutamanya bagi mereka dari keluarga berpendapatan rendah. Pada pandangan kami, ini sebaiknya dilakukan dengan memikir semula keseluruhan corak pemikiran dasar berkaitan pinjaman pendidikan, pembiayaan pendidikan tinggi, dan naratif yang memihak kepada ijazah tradisional. Kami membayangkan masa depan yang menyediakan peluang pendidikan pelbagai landasan (dan lebih murah), dan yang menjadikan simpanan pendidikan sebagai satu kelaziman sosial untuk menggalakkan pembelajaran sepanjang hayat. Mendasari perubahan corak pemikiran dasar ini adalah peringatan kami bahawa tiada lagi solusi satu saiz untuk semua (one size fits all), tetapi sebaliknya dasar-dasar awam kita patut mensasarkan bantuan yang lebih besar kepada mereka yang paling memerlukannya.

Malaysia’s current monthly minimum wage is RM1,200, increasing gradually from RM900 back when it was first implemented in 2012. By law, the next revision is supposed to occur this year. There has been talk that the government will raise it to RM1,500 a month – a significant 25% increase. This has naturally generated extremely contrasting reactions, from employers’ sharp objections, to “it’s high time” from worker groups, to divided analysts.

Whether we will see a RM1,500 minimum wage or not, one fundamental thing remains: the way the minimum wage is set and decided is and has been quite opaque. Although there is a stated ‘formula’ for revisions, the actual level of the minimum wage appears to be determined mostly through negotiations amongst key stakeholders, including the Cabinet and members of the National Wages Consultative Council (NWCC).

Yet, knowing how the minimum wage is set is critical to all working Malaysians. For the lowest paid employees, it sets the legal floor for wages and salaries. For informal workers, it stands as a rough benchmark for the minimum they should be earning from their informal jobs.

Times are changing the discussion. As early as 2018, proponents such Bank Negara Malaysia (BNM), Khazanah Research Institute (KRI) and Malaysia Trade Unions Congress (MTUC) have argued for setting the minimum wage at the level of a ‘living wage’, in other words a level which allows for a reasonable standard of living. BNM has estimated this to be RM2,700 for an unmarried individual in Klang Valley.

The push to clearly define the basis for the minimum wage grew further after the government updated the poverty line income from RM980 to RM2,208 in 2020. The pandemic and the trend of dramatic price increases also increased pressures to rethink the minimum wage.

The current policy approach of negotiating a few hundred ringgits’ increment every two years is clearly insufficient. The electioneering practice of simply promising a certain figure as the new minimum wage is also not good enough. Political parties will have to step up their policy game. In a potential election year, we ask political parties, how do they propose to address Malaysia’s minimum wage long-term? What improved promises can we expect on their manifestos?

Promise 1: From Conflicting Aims to A Clear Principle?

Since the Minimum Wage Order* was enacted in 2012, the government has reviewed the minimum wage with advice from the NWCC at least once every two years, as required by the NWCC Act 2011. Between 2012 to 2020, the minimum wage has been raised from RM900 a month for West Malaysia and RM800 for East Malaysia to RM1,200 a month for 56 municipal council areas and RM1,100 a month for other areas (Figure 1). That’s an increase of RM300 over a period of nearly a decade, which works out to an average 3.3% a year, or around an average of 1.5% annually after accounting for inflation. For reference, the average growth of Malaysia’s nominal GDP is around 6.4% during the same period (excluding 2020), or 5.1% in real terms.

*Part 2 of our Fair Work Act Research Series discussed the history of Malaysia’s Minimum Wage Order and explained the institutions behind the minimum wage in Malaysia.

Figure 1: Changes in Malaysia’s minimum wage rates since inception

Source: NWCC Act 2011; Minimum Wage Order

It is not entirely transparent what truly determines the level of the minimum wage. This is perhaps rooted in the very foundations of our minimum wage law which has two conflicting aims: firstly to ensure employees can meet basic needs and secondly, to provide a conducive environment for industrial production.

The first aim, judging by current benchmarks, seems to be of lower priority. Take the Klang Valley. The current minimum wage of RM1,200 is far lower than various ‘basic needs’ estimates, be it BNM’s living wage estimate of RM2,700 for singles, or SWRC’s reference budget level of RM1,870 for unmarried public transport users.

There is a stated minimum wage formula on the NWCC website, which incorporates relevant indicators such as the national poverty line, median income, inflation rate and more. However, judging by the quantum of minimum wage increases over the past decade and the gap between the minimum wage and the living wage, it is hard to say with confidence that the actual minimum wage has adhered to the stated formula.

And so we ask Malaysia’s political parties: What should be the principle or basis governing our minimum wage? How should it be set?

In answering this question, political parties would reveal what they think is the core purpose of a minimum wage. If parties agree that the core purpose of a minimum wage is to ensure that the lowest paid workers can meet the cost of living, the calculation of the statutory minimum wage should be based on a fixed percentage of the national median wage or a formalised calculation of a living wage, or some other clear living costs benchmark. After basic principles are established, then political parties can impress us further if they choose, for example, whether to set different minimum wages by state or region, whether to have specific sectoral provisions, and so on. But the first basic principle for setting the minimum wage is critical.

Setting the minimum wage more firmly and transparently based on a cost of living benchmark would also lend towards more gradual and more forecastable increases. While the mooted figure of RM1,500 is commendable for getting closer to living wage estimates, it is a marked 25% increase from current levels which will be very hard for some companies to bear, particularly in an economy still dealing with COVID-19.

Promise 2: From Piecemeal to Holistic Policy Thinking?

As we argued above, the minimum wage appears to be determined mostly through negotiations amongst key stakeholders. Judging by past media statements vs. the rate of minimum wage increases, it’s fair to conclude that much of the negotiations is driven by pushback from employer groups. Part of the problem here is the patchiness of complementary policy instruments that meaningfully support employers and companies, particularly MSMEs, to make the adjustment towards higher wages. Policy instruments like conditional wage subsidies, for example.

In the absence of holistic and supportive policy instruments, there will always be a high degree of objections to increasing the minimum wage. And so we would like to ask Malaysia’s political parties: how should the country improve the broader policy framework around Malaysia’s minimum wage? What other policy instruments should be implemented?

The question means to shift the policy conversation from debating piecemeal updates of minimum wage figures towards implementing the right policy model for systematic reform. As per Promise 1 above, political parties could offer to update the formula in the Minimum Wage Order to ensure closer alignment with cost of living levels. To accompany that however, complementary measures such as systematic wage subsidies should be designed and added into Malaysia’s minimum wage framework for qualifying employers and companies.

Promise 3: From Limited to Near-Full Coverage?

As digitalisation accelerates labour informalisation, more and more Malaysians are taking up new types of informal jobs, such as e-hailing and delivery gig work. This emerging class of informal workers has increasingly exposed the coverage gap of the minimum wage law. In law, only those with formal employment, whether full-time or part-time, are eligible to earn a minimum wage. While the statutory minimum wage is somewhat of a rough benchmark for informal workers’ salaries, there is no law protecting informal workers from being underpaid by employers even if they work full–time.

And so we ask Malaysia’s political parties: How should the current laws on minimum wage be amended to account for different types of informal workers?

As a start, political parties could provide the right of earning a fair minimum wage to informal workers and those without employment contracts by updating the definition of “employment” in the Employment Act 1955 as well as setting minimum conditions into the Contract Act 1950. Regardless of employment status, anyone who works for an equivalent of full-time hours should earn a salary not less than a minimum living wage.

Conclusion

The media and online ‘debates’ on the precise level of the minimum wage masks fundamental underlying policy questions regarding its purpose, model and coverage that had long been missing in Malaysia’s political discussions. In the run up to the 15th General Election, we hope that some brave and forward-thinking political parties would stop discussing minimum wage as a numbers game but instead go the extra mile to develop, communicate and promise meaningful policy reform.

Last year we began a research series to address the quandary of student debt in Malaysia, and recommended some key policy changes towards resolving problems related to outstanding loans as well as longer term systemic solutions.

Part 1 of this research series summarises the issues. Since the establishment of Malaysia’s primary student loan institution PTPTN in 1997, RM62.5 billion in student loans have been issued to 3.5 million borrowers. The success of the system hinges on broad and consistent positive returns to higher education. However, upward social mobility from higher education has not been evenly realised, putting pressure on this policy approach.

In Part 2, we advocated three bold policies to address issues related to current outstanding student debt: targeted partial debt cancellation, income-based repayment, and greater oversight on the workings and financing of PTPTN. Segmenting existing borrowers by their capacity to repay is a key pillar of these recommendations.

In Part 3, we proposed ideas for reforming the way Malaysians finance their higher education. We argued for policymakers to internalise the changing face of higher education and enact policies that evolve with recent trends. This includes diversifying from traditional degrees to TVET and microcredentials, shifting from loans to direct subsidies for students from underprivileged households, and providing individual lifelong education accounts.

In this final instalment, we present findings from our survey of student loan borrowers, which aimed to understand borrowers’ views on student loans and the impact of student loans on their lives. The majority of our survey respondents agreed that their education was worth taking out (and paying off) their student loans, and getting into debt seems to be a ‘necessary evil’ towards achieving tertiary qualifications. Nevertheless, progressive policy recommendations such as direct subsidies to underprivileged students and income-based repayment were strongly supported. At the same time, there appears to be a lack of knowledge on how PTPTN, the biggest loan provider, conducts its borrowings and lendings. These were some key findings, among many others, of our survey which is further detailed below.

About the study

The study was conducted via an online questionnaire, distributed using a convenience samplingmethod, between 3 August to 17 September 2021. The survey came in both Malay and English versions.

Since the survey’s sampling method was not stratified random sampling, results must be read with that in mind. Based on the profile of our survey respondents, we estimate that our survey respondents skew urban, but are fairly representative of student loan borrowers on other major demographic parameters such as age and gender. However, we acknowledge that this estimation can only be confirmed with access to a student loan database, which is not publicly available.

A total of 356 responses were collected during the study period of which 53 were rejected due to their status as non-borrowers and another two were excluded due to the respondents’ inconsistent or duplicated information, leaving a sample of 301 responses.

55% of the respondents were female. 73% of respondents were between 25-40 years of age, 19% were between 17-24 years old, and 8% were between 41-55 years old. Ethnically, 71% were Malays, followed by 12% Chinese, 9% Indians, and 5% non-Malay Bumiputera. Geographically, 64% of respondents came from Selangor and Kuala Lumpur.

Demographics of Survey Respondents

Employment, income and financial patterns

The majority of respondents are employed in some capacity. 68% of respondents were full-time employees, while 11% were otherwise employed as part-time employees or freelancers or entrepreneurs; 2% were full-time homemakers. Of those not in employment, 7% were unemployed and 12% were still studying. (Figure 1).

Figure 1: Employment status

With respect to current income, after excluding those who identified themselves as still studying, 9% of respondents stated that they have no regular monthly income, 16% earned less than RM2,000 a month, and 36% earned between RM2,000 and RM4,000 a month (Figure 2). Altogether, 61% of respondents earned below RM4,000 a month.

Figure 2: Current monthly income

A majority of respondents, 67%, were early-career employees with 7 years’ or under working experience. 38% of respondents reported working for less than 3 years, 29% reported between 3-7 years, 11% reported 7-10 years, and 22% reported more than 10 years (Figure 3).

Figure 3: Years of working experience

In terms of perceived income growth (again after excluding those who were still studying), we found that 42% of respondents reported steadily increasing income – a noteworthy finding that reflects positively on career progression and the returns to higher education. However, a significant 44% of respondents reported that their income has been somewhat stagnant since they started working. A minority reported worrying income trends: around 10% reported unstable income, 2% reported no income, and 3% reported decreasing income (Figure 4).

Figure 4: Respondents’ income trend

Also noteworthy: 52% of respondents reported that the Covid-19 pandemic had little to no impact to their income, while 13% even saw their income increase during this period. However, among those whose income had been disrupted, the losses were substantial; 8% saw their income decrease by at least 30%, and another 11% reported experiencing a job loss (Figure 5).

Figure 5: Impact of pandemic on income

A small majority of respondents, 54%, have at least one financial dependent such as a non-working spouse, children or parent(s) (Figure 6).

Figure 6: Number of financial dependents

Other than student loans, approximately 67% of borrowers report providing some level of financial support to their parents. 45% have car loans to service, and 30% have credit card debts to pay. 25% have housing loans, and 21% have incurred personal loans (Figure 7).

Figure 7: Type of financial obligations

What they borrowed for, and how much

The vast majority of respondents (74%) took out just one student loan, though a sizable number took out two student loans (25%) and a minority took out three student loans (1%).

Figure 8: Number of educational loans per respondent

The loans were mostly used to fund a bachelor’s degree, followed by pre-u and diploma (Figure 9).

Figure 9: Courses funded by student loans

A majority of respondents studied in public higher education institutions (IPTA) compared to private higher education institutions (IPTS) and overseas institutions. The share of overseas education amongst respondents is higher for post-graduate studies and professional/technical certification (Figure 10).

Figure 10: Type of institution by level of course type

Interestingly, respondents indicated a high completion rate of their study programs. The completion rate for bachelor’s degrees was 88%; only 2% failed to complete their programs while the remaining 10% of respondents were still studying (Figure 11).

Figure 11: Course completion rate

In terms of loan providers, PTPTN was by far the largest source of student loans. 82% of respondents reported borrowing from PTPTN, followed by 14% from MARA and 8% from state governments (Figure 12).

Figure 12: Sources of student loan

In terms of loan amount, 82% borrowed under RM60,000,which is consistent with the average loan size stated by PTPTN’s chairperson. 10% of respondents borrowed less than RM15,000 41% borrowed RM15,001 to RM30,000 while another 31% borrowed RM30,001 to RM60,000; only 7% borrowed more than RM100,000 (Figure 13).

Figure 13: Student loan amount

In terms of the length of time to fully repay their student loans per their loan agreement, 34% stated that they have to pay it off within 5-10 years and another 34% stated they will have to pay it off within 10-20 years. 16% reported they have to pay their debts within 20-30 years and the remaining 8% reported that they will take more than 30 years to pay off their student loan (Figure 14). For the record, PTPTN allows borrowers to restructure their loans which can extend the repayment period until the borrower reaches 60 years of age.

Figure 14a: Student loan tenure

Figure 14b: Student loan tenure by total loan amount

Borrowers’ monthly repayments depend on their loan size and repayment period. A large majority of respondents, 72%, pay between RM100 and RM300 a month. Of these, 8% pay less than RM100 a month, 45% of respondents pay between RM100 and RM200 a month, 27% pay between RM200 and RM300 a month, 11% pay between RM300 and RM400 a month, 5% pay between RM 400 and RM 500 a month, and 4% pay more than RM500 a month (Figure 15).

Figure 15: Monthly loan repayment amount

When borrowers’ income is commensurate with their monthly repayment and debt amount, student debt is less of a problem. Except for those who reported having no monthly income currently, monthly repayments are generally consistent with borrowers’ income level, i.e. borrowers with higher monthly loan instalments tend to earn at higher levels (Figure 16). There is however a segment of graduates earning less than RM2,000 or with no income that face considerable monthly repayments. In the highest income group, curiously 38% of those earning more than RM7,000 were paying RM200 or below in monthly repayments – another argument perhaps for setting repayment amounts based on income.

Figure 16: Monthly loan repayment by respondents’ income

41% of respondents have negotiated to restructure their loan repayment at least once – a surprisingly high number. The greater the loan size, the more likely that borrowers will restructure their loan repayment. Roughly 75% of respondents who borrowed more than RM100,000 restructured their loan repayment, followed by 46% of those who borrowed between RM60,001 to RM100,000, 40% of those who borrowed between RM30,001 to RM60,000, 40% of those borrowed between RM15,001 to RM30,000, and only 20% among those who borrowed less than RM15,000 (Figure 17).

Figure 17: Loan restructuring by loan size

In terms of their income, surprisingly, there were more respondents who restructured their loans amongst the highest income group (49% amongst those making greater than RM7,000 a month) compared to the lowest income group (26% amongst those making less than RM2,000 a month) (Figure 18)*. This may be attributed to two possible reasons: those who have higher income could perhaps afford to take advantage of PTPTN discounts for large sum repayments and so could restructure to settle their loans quicker, while those who have the least income defaulted rather than restructured their loans.

*This pattern holds even when we compare the second highest income group and the second lowest income group. The exception is those who reported no monthly income – about 50% of them restructured their loans.

Figure 18: Loan restructuring by respondents’ income

In terms of repayment rate, which has been a thorny issue generating sharply divergentheadlines, our survey mostly corroborated PTPTN’s statements: while a small minority defaults, a majority of borrowers do repay their loans. 60% of respondents can be categorised as having good standing in that they have either completely repaid their loans or are paying as scheduled. 20% can be categorised as inconsistent payers and 8% can be categorised as hardcore defaulters who never repay their loans. 12% of respondents were not yet scheduled to begin repayment (Figure 19).

Figure 19: Repayment status amongst respondents

Taking a closer look into defaulting patterns, our findings are largely confirmed by PTPTN’s own survey (mentioned in this publication here) that defaulters tend to come from low-income groups. For those who made inconsistent payments, 46% of them reported having no current income or earned less than RM2,000 a month and another 29% earned between RM2,000 and RM4,000. For those who never made repayment, 36% of them reported no monthly income currently and another 32% earned less than RM2,000. Nevertheless, there is a sizable percentage of those making inconsistent payments from high income groups: 14% of them earned between RM4,000 and RM7,000, and another 12% of them earned more than RM7,000 a month (Figure 20).

Figure 20: Repayment status by respondents’ income

To better understand motivations behind paying or not paying off student loans, we asked respondents to check a list of statements that explain their actions. The top three reported reasons why borrowers of good standing pay their loans are: they feel responsible for what they owe (94%), they do not like to be in debt (93%), and they want to avoid penalties (87%) (Figure 21).

Figure 21: Motivations for consistent repayment

Among those who did not pay or were paying inconsistently, the top three reported reasons for their payment behaviour were: they do not have enough to cover their cost of living (75%), they were waiting for announcement or election promises to discount their student loan (73%), and they believe it is unfair to have to pay this much for their education (71%) (Figure 22).

Figure 22: Motivations for inconsistent payment/defaulting

First Generation Student Loan Borrowers vs. The Rest

59% of respondents identified as first-generation tertiary graduates (‘first gens’), meaning that neither parent possesses a university degree. While this testifies to the benefit of student loans in enabling first gens to pursue higher education, they also appear to earn lower incomes, as a group, compared to borrowers with parents that have higher education qualifications.

There was a higher proportion of first-gens earning below RM2,000 (20%) compared to non first-gen respondents (11%). There were also more first-gens who reported having no monthly income currently compared to non first-gen respondents. Bottom line: even though attaining higher education is important, parents’ educational qualifications are also a determinant to a borrowers’ earning capability.

Figure 23: Income of first generation borrowers versus others

Impact of, and Perception on, Student Loans

In addition to their profiles and borrowing, we also asked respondents how they perceived the worth of student loans, the impact of student loans on their finances, and whether today’s student loan policies should be continued or reformed.

When we asked respondents if they felt that the education or qualification that they received was worth their student loans, a majority of 59% reported that it is worth it (Figure 24). Roughly 22% reported feeling neutral and the remaining 20% indicated that it was not worth it.

Figure 24: Perception of education’s worth compared to student loan

When we examined the data according to income, unsurprisingly we found that those who earned less are more likely to report that their higher education is not worth the loan compared to those who earned more. Borrowers who earned less than RM2,000 a month or had no monthly income currently were more likely to report that their education is not worth the student debt incurred compare to respondents earning at higher levels (Figure 25).

Figure 25: Perception of education’s worth by respondents’ income

When we compare perception of education’s worth by the types of institutions for bachelor’s degree – the most popular course amongst our respondents – we found that those in local public higher education institutions (IPTA) are more likely to report that their education is worth the loan compared to their peers in local private higher education institutions (IPTS). The latter was also slightly more likely to express that their education is not worth the loan. Also noteworthy: those who studied in overseas higher education institutions were more strongly inclined to report that their education is worth the loan compared to those from local higher education institutions.

Figure 26: Perception of education’s worth by type of educational institution (degrees only)

Somewhat surprisingly, relatively few respondents reported experiencing loan penalties (Figure 27). Only 11% said they experienced being unable to travel due to immigration blacklists for not repaying their student loan. 4% reported being sued for not repaying student loans, and another 2% reported that they declared court bankruptcy for not repaying their student loans. 24% reported difficulties in getting a bank loan because of their student loan repayment status affecting their creditworthiness scores.

Figure 27: Penalties faced by loan borrowers

To better understand the different ways student debt affects borrowers’ lives, we asked respondents about the impact of student loans on their finances and life plans. 59% reported that student loans contributed to financial stress, 57% reported that student loans contributed to a delay in purchasing a home, and 52% reported that student loans contributed to them postponing savings, including emergency savings and retirement savings (Figure 28). 46% of respondents reported that student loans have contributed to them not starting a business or pursuing risky ventures, while 42% reported that student loans have contributed to them delaying marriage or having kids.

Figure 28: Effect of student loans on life choices

We also asked respondents what they think of some ideas to reform student loan policies. Income was a strong theme. 82% of respondents agreed that student debt is not a problem if graduates earn higher wages. Relatedly, there is strong support from respondents, 81%, to only begin student loan repayments after reaching an affordable level of income, a policy which we advocated in Part 2 of this research series. More than two-thirds of respondents, 77%, agree that underprivileged and overburdened borrowers should have part of their student loan forgiven, a proposal that we also pushed for.

Figure 29: Support for income-based repayment and partial loan cancellation

Policy ideas to impose more restrictions on student loans did not resonate with the respondents, going against our policy recommendations in this area. A majority of respondents disagree that criteria for student loans should be tightened and given for certain courses only (69%) or certain institutions only (71%), which were two of the policy recommendations we advocated in Part 3 of this research series. A small majority of respondents also reacted negatively to our policy recommendation that there should be less student loans for university degrees, and more for technical and online courses including micro-credentials (52% disagreed). That said, further studies that include a more representative sample, including more of TVET graduates, may present findings that are less skewed towards university degrees.

Figure 30: Support for loan reform proposals

77% of respondents agree that youth should not need to get into debt to attain higher education, and an even bigger majority, 82%, said the poor should not have to do so. A majority of respondents, 59%, disagreed with the statement that an individual person or family is fully responsible to save up and pay for their own higher education. Given these numbers, we would be interested to see if borrowers feel that the family should be partially responsible for paying the costs of higher education – perhaps in a future study.

Figure 31: Views on higher education financing

On the question of fiscal affordability, about two-thirds of respondents, 69%, think the country can afford to make higher education free for everyone, which in our view reflects the gulf between policymakers (who tend to be more fiscally mindful/conservative) with the general public.

Figure 32: Views on affordability of free higher education

However, many respondents were not aware of how PTPTN – the biggest loan provider – operates (Figure 33). Only 39% were aware that PTPTN borrows from financial institutions and markets. More than two-thirds of respondents, 77%, thought that PTPTN is completely funded by the government and taxpayers, and only 36% were aware that the Malaysian government guarantees PTPTN’s debts. About 40% thought that PTPTN is completely funded by the ongoing collection of outstanding loans. (We covered how PTPTN operates in Part 1).

Figure 33: Knowledge of PTPTN’s funding base

Conclusion

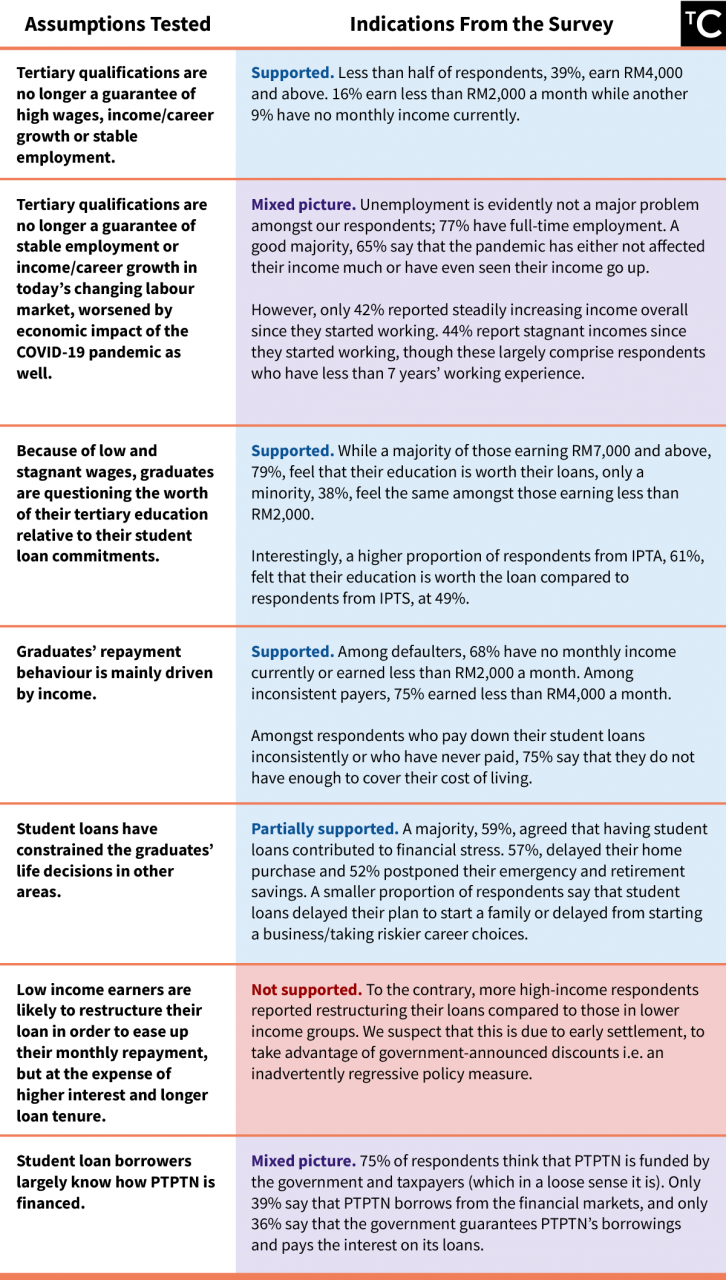

We began this research series by outlining the major problems with student loans as the main policy approach to finance one’s higher education. As have been pointed out elsewhere, a major issue is the uneven returns from higher education. This is borne out by our survey where less than half of respondents are earning RM4,000 a month and above.

Due to uneven returns from higher education, we hypothesised that graduates are questioning the worth of their tertiary education relative to their loans. This was somewhat supported by the survey, where a small majority of respondents, 59%, agreed that their education was worth the loans incurred. Borrowers whose income is lower than RM2,000 a month were especially likely to question the worth of their tertiary education.

We tested our other assumptions on related facets such as payment behaviour, level of loan restructuring, how student loans affect stress and life plans as well as the extent of knowledge on how PTPTN is financed; these are summarised in Table 1 below. While we were mostly validated regarding the effects of income on some of these hypotheses, some results were less negative/severe than we expected.

Table 1: Assumptions tested and indications from the survey

Apart from the assumptions above, we also tested our policy perspectives against borrowers’ views via the survey (Table 2). Some of our policy recommendations did not find favour. In Part 3, we had advocated to tighten conditions and limit student loans to certain courses or institutions with proven track records, but respondents rejected this proposal by a huge margin. We had also advocated to extend more student loans for technical and vocational (TVET) and microcredit courses but respondents were not enthusiastic about reducing loans for traditional degrees in favour of funding more TVET and microcredit courses.

However, other proposals evidently struck a chord among the respondents. There was strong endorsement to permit borrowers to begin repayment only after they reached an affordable level of income i.e. income-based repayment. Respondents also supported our policy view that lower income households should not have to incur debt to attain higher education, suggesting an appetite for progressive reforms. Our policy recommendations that align with such a vision include providing targeted and partial student loan cancellation for low income borrowers as well as direct subsidies, rather than loans, to low-income students.

Table 2: Support for our loan policy recommendations