Since 2005, many Malaysian companies do not directly hire migrant workers. Instead, migrant workers are employed by recruitment agencies, which in turn outsource them to the companies.

This outsourcing practice was institutionalised through a 2012 amendment of the Employment Act 1955. Under this system, work permits are attached to the recruitment agents, or “contractors for labour”, instead of the companies which the migrant workers are outsourced to. Companies prefer this arrangement as workers who are not direct employees would not be subject to collective bargaining agreements and can be hired for specific periods of time and be sent back to the recruitment agencies once their services are no longer needed. The system has also distanced the companies from any liability towards the workers.

Critics have highlighted how the system has brought back labour practices that are reminiscent of those from the British colonial era, which deprived workers of their basic rights. Many of the workers have found themselves in debt bondage from having paid high recruitment fees to the agencies. They have also been subjected to numerous forms of mistreatments, including the withholding of passports by employers, and exposure to poor working conditions.

Who and what is involved in the recruitment process?

To hire foreign workers, the company first needs to obtain a letter from the Ministry of Human Resources’ (MOHR) Jabatan Tenaga Kerja Semenanjung Malaysia (JTKSM) confirming that they are not able to hire Malaysian workers.*

Part of the process involves putting up a job posting on the JobsMalaysia online portal (replaced by MYFutureJobs on 1 November 2020) to advertise available vacancies to local workers. For several years there was no fixed time period for advertising on JobsMalaysia in order to determine that no Malaysians can fill the vacancies. Companies treated the requirement as a formality and would proceed to apply for foreign workers via MOHR’s Sistem Permohonan Pekerja Asing (or ePPAx) right after posting the vacancies on JobsMalaysia. In June 2020, however, a 30-day mandatory posting period was added through a cabinet decision.

* The approver for Sabah is the Sabah State Labour Department and the Committee for Foreign Workers in Sabah and Labuan, and for Sarawak is the Sarawak State Labour Department.

With the letter from JTKSM, the company can apply for a foreign worker quota from MOHR. The Ministry will approve the application if the company meets the relevant criteria.

This quota is a company-specific quota for a certain position that was posted on JobsMalaysia which Malaysians could not fill. The job posting allows the company to apply for a certain number of foreign workers for the position. This is the first among two quotas that the company needs to apply for, the second being the one issued by the Ministry of Home Affairs (MOHA). The quotas can also be applied for through a recruitment agency, who may act on behalf of the company throughout the recruitment process.

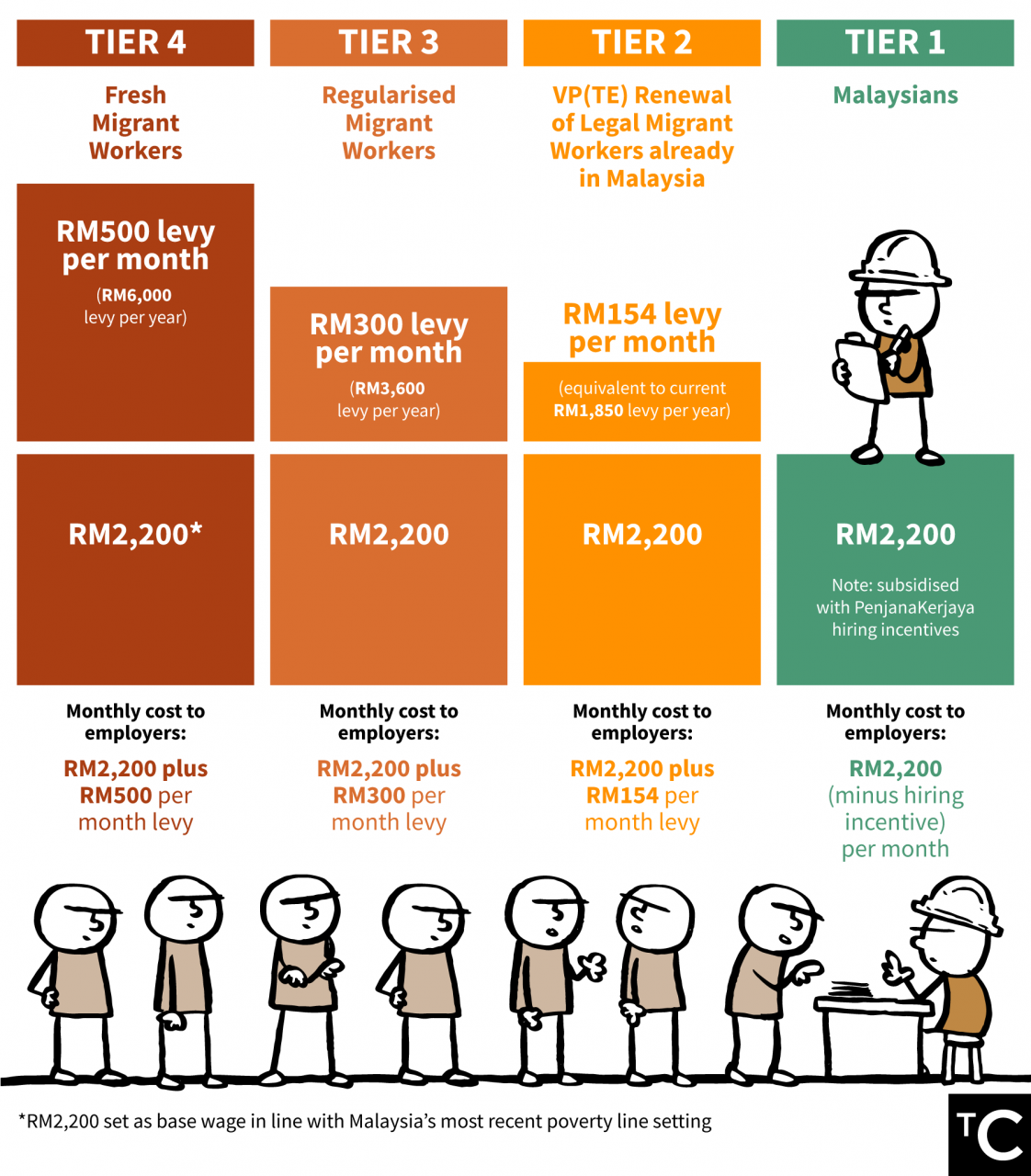

Once the company has obtained the approval from MOHR, it can apply to MOHA for the Ministry’s foreign worker quota. This is typically an online process via the Foreign Workers Centralized Management System (FWCMS). Once the quota is approved, the company needs to pay the workers’ levy*, the relevant insurance policies, and a security bond.

Quota allocation is determined by MOHA based on a list of approved “source countries” and specific industries in which workers from those countries are allowed to work. Quotas are determined by arbitrary guesstimates based on different industry guidelines. For example, for the plantation sector, guidelines from the Ministry of Plantation Industries and Commodities may indicate 1 foreign worker for every 8 hectares of palm oil plantation, while for the construction sector, guidelines from the Construction Industry Development Board indicate 1 foreign worker for every 3 Malaysians. Meanwhile, in the services sector, 5-star hotels are allowed to hire 1 foreign worker per 12 rooms, while 1-star hotels can hire 1 foreign worker per 30 rooms.

* Introduced in 1992 with multiple increases since, levies were originally imposed on migrant workers in order to cover their use of public services and infrastructures. The levies yielded approximately RM1.75bn to RM2.75bn to the government annually between 2005 to 2014.

Once the relevant quotas have been approved, the company can begin recruiting. However, this is not an easy process. For companies that require the services of a large number of workers, it is logistically challenging and uneconomical for them to internalise the recruitment process. They will instead enter into a contractual agreement with the recruitment outsourcing agency, which will not only help find the migrant worker candidates from the source country, but which will also become the workers’ direct employers.

To find the worker candidates, the outsourcing agencies typically engage the services of agents that are based in the targeted countries. Upon receiving a request from the destination country, the agents, however, may find it difficult to locate prospective migrants from remote areas and villages; they also charge an upfront recruitment fee and will need to find people who would be willing to pay the fee in order to get hired. To facilitate the process, the agents rely on informal sub-agents to act as intermediaries between them and the prospective workers.

The informal sub-agents assist in the process by vouching for the recruiters and convincing the prospective migrants to migrate. They also assist in the paperwork, passport application, bank account opening, medical check-up, and transportation to the airport for the would-be migrant workers. In some cases they even act as guarantors for the workers who require credit. Many intermediaries are in fact returnee migrants or relatives of prospective migrants who are familiar with the procedures and challenges of migration. This stage of the recruitment process can prove to be costly for the worker, as we will discuss further below.

Once the services of the workers are secured, the outsourcing agency applies for a Visa With Reference (VDR) at the Malaysian Embassy in the source country so the workers can travel to Malaysia. Upon arrival in Malaysia, the workers have 30 days to undergo a medical checkup by the Foreign Workers’ Medical Examination Monitoring Agency (FOMEMA) Sdn Bhd.

The medical checkup is usually arranged by the employer. Once the workers have obtained the medical clearance, the employer can then apply for an employment pass called the Visitor Pass (Temporary Employment), or VP(TE). After receiving the VP(TE) the workers can begin their employment in Malaysia.

Despite this being the formal process, employers can also bypass it through Special Approvals (Kelulusan Khas) from the Ministry of Home Affairs through ministerial approval and ‘intermediaries’. Between 2016 and 2018, a quota totalling 512,315 was approved by MOHA or through special committees, instead of going through JobsMalaysia, which approved 416,510 foreign workers over the same period. Through Special Approvals, 22,901 foreign workers were allowed to work in Malaysian-only sectors and of the 7,784 employers granted Special Approvals, only 1,036 advertised the jobs on JobsMalaysia.

The employer is also legally liable if the migrant workers abscond and become illegal. Abscondment is reported as the second largest challenge that employers face in dealing with migrant workers, after communication problems. In the event of abscondment, in order to cancel the VP(TE), the employer will need to submit documentation to the Malaysian Immigration Department which includes the foreign workers’ passports.

In order to mitigate the risk of abscondment, the passports (and the VP(TE) inside) are often held by the recruitment agency or company, even if the government has made it clear that this an offence under the Passport Act 1966. There have also been reports of employers attempting to compromise by storing passports on premise with the workers keeping the key, in response to pressures from multinational companies.

The status of recruitment agencies through the years

The legality of recruitment agencies in Malaysia has been subject to numerous policy U-turns. They were first legalised in 1981 through the Private Employment Agencies Act. Due to exploitation, indenture, corruption and fraud, they were subsequently banned in 1995 and were replaced by a Special Task Force on Foreign Labour under the Ministry of Home Affairs as the sole agency responsible for foreign labour recruitment. This signalled a shift to the implementation of a Government to Government (G2G) model*, which centralised foreign worker recruitment in Malaysia.

Recruitment agencies were re-legalised in 2005 through an amendment to the Private Employment Agencies Act, as lawmakers found that the ban did not solve the problem as foreign workers and employers continued to use the agencies. Moreover, the ban also made it difficult to control unregulated private agencies. This move also enabled outsourcing to be practiced in the recruitment process. From 2010 onwards, however, the government phased out outsourcing firms and reverted to the G2G model. This policy shifted again in 2012 as a result of the amendment of the Employment Act 1955, through which the concept of “contractor for labour” was invented.

During its tenure, the Pakatan Harapan government announced that outsourcing agencies would be abolished by March 2019 and companies would need to absorb the workers who they employed via the agencies. Whether or not the policy is still in place, however, is not clear. At present, due to the ongoing COVID-19 pandemic, the Perikatan Nasional government has introduced a freeze on the hiring of foreign workers.

* G2G agreements and MOUs between Malaysia and the source country are usually signed in order to cut out the exorbitant fees charged by recruitment agents from the hiring process.

The cost of working abroad for a migrant worker in Malaysia

For a migrant worker to come and work in Malaysia, a hefty amount needs to be paid. Recruitment agencies and sub-agents may charge each worker an upfront recruitment fee that can be multiples of the actual cost of the expenses it is meant to cover. A large proportion of the workers end up having to sell land or property or take on debt to finance the migration at usurious rates.

Alternatively, recruitment agencies may bear the cost of recruitment, but often recoup the outlay through salary deductions once the workers have been outsourced to other companies. These fees are only meant to be paid once; however, researchers have found that some agents in the source countries double-dip, claiming the same expenses from both the worker and the employer in Malaysia.

Many migrant workers become indentured as a result of this. If a worker comes to Malaysia to work for an average salary of RM1,000 a month, the indenture would be worth 20 months wages in the case of a Bangladeshi, 5-6 months for a Nepali, and 2-3 months for an Indonesian. For Nepalis and Indonesians, there is some semblance of financial viability with extreme scrimping. However, the reality is that Indonesian maids have reported needing to pay 6-10 months of their wages to recruitment agencies. For Bangladeshis, the payback is gravely uncertain because the VP(TE) is only issued for 12 months with a possibility of additional 12-month extensions for up to 10 years, which are not guaranteed. Taking into account living costs, interest on the loan, potential employer salary deductions and a reasonable profit, there is a built-in assumption that Bangladeshi migrant workers will need to work in Malaysia continuously for several years, whether legally or otherwise, before seeing any semblance of a financial return.